How Blockchain Technology Works Guide for Beginners

Blockchain technology is a decentralized digital ledger that records transactions across multiple computers. It works through a network of nodes that validate and store information in blocks, creating a secure and transparent record of transactions.

Welcome to the beginners' guide to understanding how blockchain technology works. We'll explore the basic principles behind blockchain, its key components, and the process of transaction verification.

By the end, you'll have a clear understanding of the fundamental concepts of blockchain technology and its potential applications in various industries. So, let's dive into the world of blockchain and demystify its workings for beginners.

What Is Blockchain Technology

Blockchain technology is a decentralized, distributed ledger system that securely records transactions across a network of computers.

Definition Of Blockchain

A blockchain is a chain of blocks containing digital information that is linked and secured using cryptography.

Key Features

- Decentralization: No central authority controls the blockchain network.

- Transparency: All transactions are recorded on a public ledger for anyone to view.

- Immutability: Once data is added to the blockchain, it cannot be altered or deleted.

- Security: Consensus mechanisms like Proof of Work ensure the integrity of the network.

- Smart Contracts: Self-executing contracts based on predefined rules automate transactions.

How Does Blockchain Work

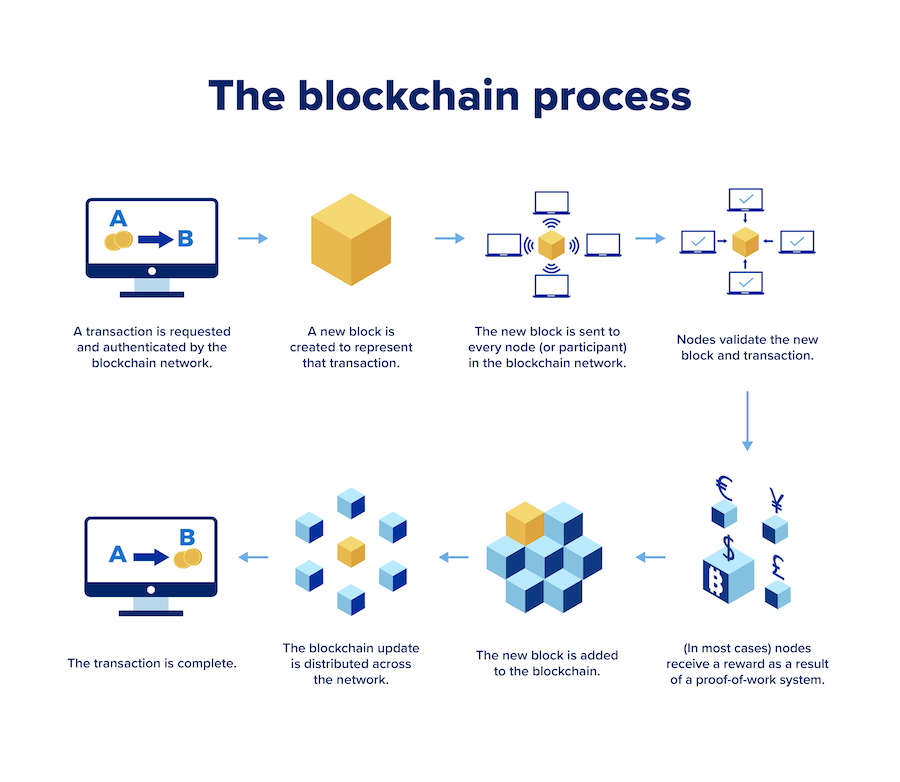

Blockchain technology is a revolutionary system that securely records and verifies digital transactions in a decentralized and transparent manner. By using a network of computers, each transaction is added to a "block" and linked in a chain, making it virtually impossible to alter or manipulate the data.

As a beginner's guide, this article explains the key principles and processes behind how blockchain works.

Introduction: In this section, we will dive into understanding how blockchain technology works. Blockchain has gained significant attention in recent years for its potential to revolutionize numerous industries.Components Of A Blockchain

Blockchain technology comprises various components that work together to ensure the security and transparency of the system. Understanding the fundamental elements of a blockchain is essential for beginners. Let's delve into the components of a blockchain, including blocks, nodes, and smart contracts.

Blocks

A block is the basic building unit of a blockchain. It contains a list of transactions and a unique identifier known as a hash. Each block is linked to the previous one, thereby forming a chain, hence the term "blockchain." Blocks also contain a timestamp and other relevant information that enhances the security and integrity of the blockchain network.

Nodes

Nodes are individual devices or computers connected to the blockchain network. They play a crucial role in maintaining the decentralized nature of the blockchain. Each node stores a complete copy of the blockchain and participates in validating and relaying transactions. This redundancy helps to uphold the security and resilience of the overall system.

Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. These contracts automatically facilitate, verify, or enforce the negotiation or performance of a contract, enabling trust and transparency without the need for intermediaries. They are a cornerstone of many blockchain platforms, allowing for the creation of various decentralized applications and services.

Credit: www.plainconcepts.com

Types Of Blockchains

Blockchain technology comes in various types such as public, private, and consortium blockchains. Each type has unique features suited for different applications and industries. Beginners can explore these different types to understand how blockchain technology works and its potential benefits.

Types of Blockchains Public Blockchain A public blockchain is a decentralized blockchain, and it allows anyone to participate, read, write, and audit the blockchain. It is accessible to anyone who wants to be part of the network.Benefits Of Blockchain Technology

Blockchain technology has revolutionized numerous industries with its distinct advantages. Understanding the benefits of blockchain technology can help beginners grasp its potential and impact. This guide will explore the key advantages of this revolutionary technology, including its transparency and immutability, enhanced security, and efficiency and speed.

Transparency And Immutability

One of the significant benefits of blockchain technology is its inherent transparency. Blockchain is a decentralized ledger that records all transactions across a network of computers known as nodes. Each transaction is added to a block, which is then linked to the preceding block, creating a chain of information.

This distributed ledger ensures that every network participant has access to the same information. This transparency eliminates the need for intermediaries, such as banks or financial institutions, enabling users to directly engage in peer-to-peer transactions. Moreover, all transactions recorded on the blockchain are immutable, meaning they cannot be altered or tampered with once they are added to the chain.

Enhanced Security

Blockchain technology offers enhanced security, making it highly resistant to fraud and unauthorized changes. The decentralized nature of blockchain eliminates the reliance on a centralized authority, reducing the risk of a single point of failure or corruption. To compromise the integrity of the blockchain, an attacker would need to control the majority of the network's computers, which is highly unlikely in a well-established blockchain network.

Additionally, blockchain employs advanced cryptographic techniques to secure transactions. Each transaction is sealed with a digital signature, ensuring that it can only be verified by the intended recipient. The use of cryptographic hashes further enhances security by creating a unique identifier for each block, making it nearly impossible for malicious actors to alter previous transactions without having to modify all subsequent blocks.

Efficiency And Speed

Another notable benefit of blockchain technology is its efficiency and speed. Traditional financial systems often involve numerous intermediaries and complex processes that can slow down transactions. However, blockchain removes the need for intermediaries, enabling faster and more streamlined transactions.

Moreover, blockchain technology operates 24/7, allowing transactions to be processed at any time of the day without delays. This can be particularly beneficial in global transactions, as it eliminates time-zone constraints and reduces reliance on banking hours.

In addition to speed, blockchain offers improved efficiency by automating processes and reducing paperwork. By using smart contracts, predefined rules and conditions can be coded directly into the blockchain, automating various tasks and eliminating the need for manual input. This automation increases accuracy, reduces errors, and streamlines operations.

Overall, the benefits of blockchain technology are vast and extend across various industries. Its transparency and immutability ensure trust and accountability, while enhanced security protects against fraud and unauthorized changes. Additionally, the efficiency and speed of blockchain streamline processes and improve overall operations. Embracing blockchain technology can lead to innovative solutions and transformative changes in many sectors.

Challenges In Blockchain Technology

Blockchain technology encounters several challenges that impact its widespread adoption and efficiency.

Scalability

Scalability in blockchain involves the ability to handle a large number of transactions promptly.

Interoperability

The interoperability challenge refers to the seamless interaction between different blockchain platforms.

Regulatory Uncertainty

Regulatory uncertainty creates obstacles for blockchain implementation due to inconsistent laws and guidelines.

Real-world Applications Of Blockchain

Blockchain technology offers practical uses across industries, from secure transactions in financial services to transparent supply chains in logistics. Beginners can grasp its concept and potential by understanding its decentralized structure and immutable ledger system. Explore real-world applications to see how blockchain is revolutionizing data management.

In the real world, blockchain technology is being widely adopted across various industries for its secure and transparent nature. Let's explore some key applications where blockchain is making a difference:

Credit: www.linkedin.com

Future Trends In Blockchain Technology

In this section, we'll explore the future trends in blockchain technology and how it is set to revolutionize various industries, including Integration with IoT, Cross-Industry Collaboration, and Scalability Solutions.

Integration With Iot

The integration of blockchain with the Internet of Things (IoT) is paving the way for more secure and efficient data transmission and storage. By leveraging blockchain's inherent security features, IoT devices can securely communicate and transact with each other, creating a trusted and tamper-proof network.

Cross-industry Collaboration

Blockchain technology is breaking down industry silos by enabling seamless collaboration and data sharing across different sectors. Through decentralized and transparent networks, businesses can streamline processes, reduce costs, and improve trust among collaborators through immutable records and smart contracts.

Scalability Solutions

As blockchain adoption continues to grow, scalability remains a key focus for developers and innovators. Solutions such as sharding, layer 2 protocols, and improved consensus mechanisms are addressing the scalability challenges, allowing blockchain networks to handle a larger volume of transactions without compromising security or speed.

Credit: bootcamp.cvn.columbia.edu

Frequently Asked Questions On How Blockchain Technology Works Guide For Beginners

What Is Blockchain Technology?

Blockchain technology is a decentralized, distributed ledger system that facilitates secure and transparent transactions.

How Does Blockchain Ensure Security?

Blockchain ensures security through encryption, consensus algorithms, and decentralized data storage.

What Are The Advantages Of Blockchain?

Advantages of Blockchain include transparency, immutability, decentralization, and increased security in transactions.

Can Blockchain Be Used In Multiple Industries?

Yes, Blockchain has applications in finance, healthcare, supply chain, voting systems, and more industries.

How Can Beginners Get Started With Blockchain?

Beginners can start by learning the basics of Blockchain, understanding its applications, and exploring online resources and courses.

Conclusion

To sum up, understanding how blockchain technology works is crucial for beginners in today's digital era. By providing a decentralized and secure system for recording transactions, blockchain has the potential to revolutionize various industries. From finance to supply chain management, the possibilities are endless.

As you delve deeper into this technology, remember to stay updated with the latest advancements and embrace the opportunities it brings. Start exploring blockchain today and be a part of the future of innovation and trust.